기본적으로 아래처럼 한다.

cname <- c("x1", "x2", "x3","x4", "x5", "x6", "y")

german = read.table("c:\\data\\german1.txt", col.names = cname)

options(contrasts = c("contr.treatment", "contr.poly"))

german.object <- glm(y~.,family=binomial, data=german)

summary(german.object)

p <- predict(german.object, german, type="response")

german <- cbind(german, p)

head(german)

p는 y=1일 확률이다. 교제에서는 y=1이 불량고객이다.

> head(german)

x1 x2 x3 x4 x5 x6 y p

1 A11 6 A34 4 67 1 0 0.18170622

2 A12 48 A32 2 22 1 1 0.63312134

3 A14 12 A34 3 49 2 0 0.04812842

4 A11 42 A32 4 45 2 0 0.64393801

5 A11 24 A33 4 53 2 1 0.47102819

6 A14 36 A32 4 35 2 0 0.20127115

4 변수선택법 #

전진선택, 변수소거, 둘다

cname <- c("x1", "x2", "x3","x4", "x5", "x6", "y")

german = read.table("c:\\data\\german1.txt", col.names = cname)

#상수항만 포함한 초기모형

g.object <- glm(y~1, family=binomial, data=german)

#전진선택법

s.list <- list(upper = update(g.object, ~. +x1+x2+x3+x4+x5+x6))

step(g.object, scope=s.list, direction="forward")

#변수소거법

#s.list <- list(lower = update(g.object, ~. -x1-x2-x3-x4-x5-x6))

#step(g.object, scope=s.list, direction="backward")

#둘다

#s.list <- list(upper = update(g.object, ~. +x1+x2+x3+x4+x5+x6), lower = update(g.object, ~. -x1-x2-x3-x4-x5-x6))

#step(g.object, scope=s.list, direction="both")

결과

> step(g.object, scope=s.list, direction="forward")

Start: AIC=1223.73

y ~ 1

Df Deviance AIC

+ x1 3 1090.4 1098.4

+ x3 4 1161.3 1171.3

+ x2 1 1177.1 1181.1

+ x5 1 1213.1 1217.1

<none> 1221.7 1223.7

+ x6 1 1221.7 1225.7

+ x4 1 1221.7 1225.7

Step: AIC=1098.39

y ~ x1

Df Deviance AIC

+ x2 1 1051.9 1061.9

+ x3 4 1053.2 1069.2

+ x5 1 1085.0 1095.0

<none> 1090.4 1098.4

+ x4 1 1090.2 1100.2

+ x6 1 1090.3 1100.3

Step: AIC=1061.9

y ~ x1 + x2

Df Deviance AIC

+ x3 4 1022.6 1040.6

+ x5 1 1046.7 1058.7

<none> 1051.9 1061.9

+ x4 1 1051.5 1063.5

+ x6 1 1051.9 1063.9

Step: AIC=1040.58

y ~ x1 + x2 + x3

Df Deviance AIC

+ x5 1 1019.3 1039.3

<none> 1022.6 1040.6

+ x6 1 1022.5 1042.5

+ x4 1 1022.5 1042.5

Step: AIC=1039.27

y ~ x1 + x2 + x3 + x5

Df Deviance AIC

<none> 1019.3 1039.3

+ x4 1 1019.2 1041.2

+ x6 1 1019.3 1041.3

Call: glm(formula = y ~ x1 + x2 + x3 + x5, family = binomial, data = german)

Coefficients:

(Intercept) x1A12 x1A13 x1A14 x2

0.66510 -0.53186 -1.07608 -1.89880 0.03434

x3A31 x3A32 x3A33 x3A34 x5

-0.09915 -0.94696 -0.93433 -1.52607 -0.01277

Degrees of Freedom: 999 Total (i.e. Null); 990 Residual

Null Deviance: 1222

Residual Deviance: 1019 AIC: 1039

>

최종적으로 glm(formula = y ~ x1 + x2 + x3 + x5, family = binomial, data = german) 가 선택되었다. AIC가 가장 적은 모델이 선택된다.

참고: AIC (

![[http]](/moniwiki/imgs/http.png) 출처(http://blog.naver.com/pinokio129?Redirect=Log&logNo=80018702687)

출처(http://blog.naver.com/pinokio129?Redirect=Log&logNo=80018702687))

AIC 통계량

최적 모형을 결정하는 경우 모형의 설명능력과 모형의 절약성을 고려해야 함.

모형의 설명능력은 우도(likelihood)로서 측정될 수 있으며,

모형의 절약성은 복잡한 모형 보다는 간결한 모형이 선호되어야 한다는 것으로

추정 계수의 數가 많은 것에 대해 벌칙을 가함으로써 고려될 수 있다.

그러나 모형의 설명력과 절약성은 상충되는(trade-off)기준으로서,

왕왕 복잡한 모형이 설명력이 큰것을 발견 할 수 있다.

따라서 두 판단기준을 함께 고려한 선택규준이 필요하게 된다.

그것이 바로 정보기준 접근법으로 Akailke에 의하여 개발된

Akaike Information Criterion(AIC)이다.

AIC = -2 log L +2n

여기서 'n': 파라미터 수를 나타내며, 'log L'은 대수우도(log-likelihood).

※ Akailke에 의하면 AIC통계량의 값이 최소가 되는 모형을 채택하여야 된다

D(Deviance)는 일반화된 선형 모형에서 모형의 적합도 검증 통량이다.

cname <- c("x1", "x2", "x3","x4", "x5", "x6", "y")

german = read.table("c:\\data\\german1.txt", col.names = cname)

options(contrasts = c("contr.treatment", "contr.poly"))

german.object <- glm(formula = y ~ x1 + x2 + x3 + x5, family = binomial, data = german)

summary(german.object)

결과

Call:

glm(formula = y ~ x1 + x2 + x3 + x5, family = binomial, data = german)

Deviance Residuals:

Min 1Q Median 3Q Max

-1.7997 -0.8007 -0.4747 0.9283 2.4241

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 0.665099 0.476311 1.396 0.162607

x1A12 -0.531864 0.185402 -2.869 0.004121 **

x1A13 -1.076082 0.336956 -3.194 0.001405 **

x1A14 -1.898800 0.206314 -9.203 < 2e-16 ***

x2 0.034342 0.006329 5.426 5.76e-08 ***

x3A31 -0.099153 0.474942 -0.209 0.834629

x3A32 -0.946961 0.370644 -2.555 0.010622 *

x3A33 -0.934327 0.433303 -2.156 0.031061 *

x3A34 -1.526069 0.393754 -3.876 0.000106 ***

x5 -0.012765 0.007091 -1.800 0.071821 .

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 1221.7 on 999 degrees of freedom

Residual deviance: 1019.3 on 990 degrees of freedom

AIC: 1039.3

Number of Fisher Scoring iterations: 4

숫자형 변수인 경우 분포를 보고 후보를 선택할 수 있다. (Y님이 알려준거다)

# r: 결과set

# r에서 숫자형 자료만 선별해서 plotting

# column이 숫자형인지 T/F 저장

training <- sqlQuery(conn, "select

cnt x1

, logkind x4

, genre x5

, diff_cnt x6

, diff_time x8

, gamecd x9

, reg_hh x10

, case when t <= 2 then 1 else 0 end y

from temp.dbo.out_data01

")

#install.packages("reshape")

#install.packages("ggplot2")

library("reshape")

library("ggplot2")

number_cols <- sapply(training, is.numeric)

r.lng <- melt(training[,number_cols], id="y") # id: 종속변수명.

p <- ggplot(aes(x=value, group=y, colour=factor(y)), data=r.lng)

p + geom_density() + facet_wrap(~variable,scale="free")

결과는 다음 그럼과 같다.

여기에서는 그림을 보고 x6, x8이 선택되었다.

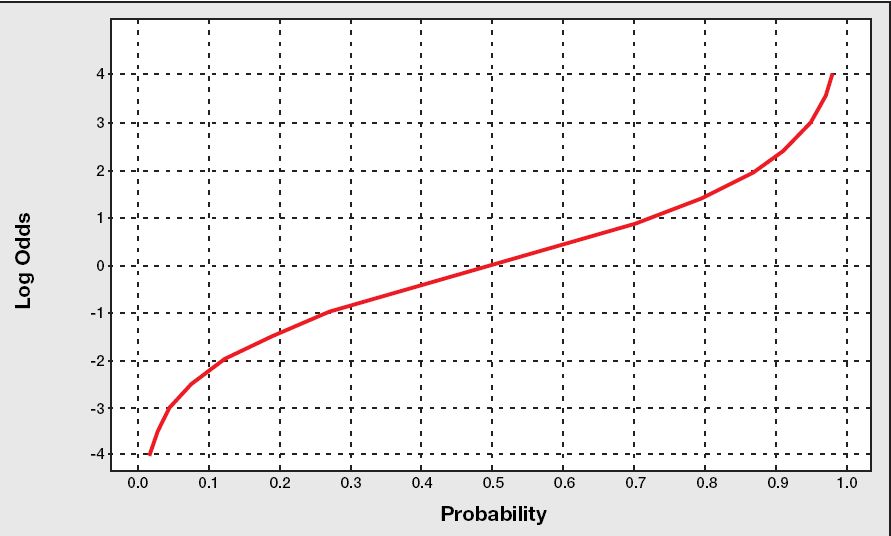

5 odds와 logit #

승산(그림 출처 ->

여기(http://www.bisolutions.us/Credit-Risk-Evaluation-of-Online-Personal-Loan-Applicants-A-Data-Mining-Approach.php))

로짓(그림 출처 ->

여기(http://www.bisolutions.us/Credit-Risk-Evaluation-of-Online-Personal-Loan-Applicants-A-Data-Mining-Approach.php)) = log와 odds를 합친말 = log(1/(1-p))

pred <- predict(german.object, german, type="response")

logodds <- predict(german.object, german)

german <- cbind(german, pred) #확률

german <- cbind(german, logodds) #오즈, odds

head(german)

결과

> head(german)

x1 x2 x3 x4 x5 x6 y pred logodds

1 A11 6 A34 4 67 1 0 0.18091034 -1.5101920

2 A12 48 A32 2 22 1 1 0.63503244 0.5538676

3 A14 12 A34 3 49 2 0 0.04865313 -2.9731627

4 A11 42 A32 4 45 2 0 0.64246423 0.5860757

5 A11 24 A33 4 53 2 1 0.46964395 -0.1215737

6 A14 36 A32 4 35 2 0 0.19922819 -1.3911252

2번째 Row는

| x1 | x2 | x3 | x4 | x5 | x6 | y |

| A12 | 48 | A32 | 2 | 22 | 1 | 1 |

이고, 회귀식이 다음과 같으므로

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 0.665099 0.476311 1.396 0.162607

x1A12 -0.531864 0.185402 -2.869 0.004121 **

x1A13 -1.076082 0.336956 -3.194 0.001405 **

x1A14 -1.898800 0.206314 -9.203 < 2e-16 ***

x2 0.034342 0.006329 5.426 5.76e-08 ***

x3A31 -0.099153 0.474942 -0.209 0.834629

x3A32 -0.946961 0.370644 -2.555 0.010622 *

x3A33 -0.934327 0.433303 -2.156 0.031061 *

x3A34 -1.526069 0.393754 -3.876 0.000106 ***

x5 -0.012765 0.007091 -1.800 0.071821 .

다음과 같이 계산된다.

0.665099 -0.531864 + 48 * 0.034342 - 0.946961 -0.012765 * 22 = 0.5538676

확률은..

x <- 0.665099 -0.531864 + 48 * 0.034342 - 0.946961 -0.012765 * 22

1 / (1 + exp(-x)) #결과값 0.6350307

exp(x) / (1 + exp(x)) #결과값 0.6350307, 이게 로지스틱 모형

과 같이 계산하면 된다.

8 분류표(confusion matrix) #

#T1 <- length(german[german$y==1 & german$pred > 0.5,]$x1)

#T0 <- length(german[german$y==0 & german$pred > 0.5,]$x1)

#F1 <- length(german[german$y==1 & german$pred <= 0.5,]$x1)

#F0 <- length(german[german$y==0 & german$pred <= 0.5,]$x1)

#

install.packages("SDMTools")

library("SDMTools")

confusion.matrix(german$y,german$pred,threshold=0.5)

결과

> confusion.matrix(german$y,german$pred,threshold=0.5)

obs

pred 0 1

0 629 177

1 71 123

attr(,"class")

[1] "confusion.matrix"

| | False(실제) | True(실제) |

| False(예측) | 629 | 177 |

| True(예측) | 71 | 123 |

| 항목 | 계산 | 확률(%) |

| 정확도 (Accuracy) | (629 + 123) / (629 + 177 + 71 + 123) | 75.20% |

| 민감도 (sensitivity) | 123 / (177 + 123) | 41.00% |

| 특이도 (specificity) | 629 / (629 + 71) | 89.86% |

| 오류율 (error) | (177 + 71 ) / (629 + 177 + 71 + 123) | 24.80% |

다음과 같이 R로 계산해도 된다.

library("SDMTools")

mat <- confusion.matrix(german$y,german$pred,threshold=0.5)

mat

omission(mat)

sensitivity(mat)

specificity(mat)

prop.correct(mat)

결과

> mat

obs

pred 0 1

0 629 177

1 71 123

attr(,"class")

[1] "confusion.matrix"

> omission(mat)

[1] 0.59

> sensitivity(mat)

[1] 0.41

> specificity(mat)

[1] 0.8985714

> prop.correct(mat)

[1] 0.752

>

다음과 같이 하면 다 나온다.

> accuracy(german$y,german$pred,threshold=0.5)

threshold AUC omission.rate sensitivity specificity prop.correct Kappa

1 0.5 0.6542857 0.59 0.41 0.8985714 0.752 0.3432203

>

값에 대한 설명

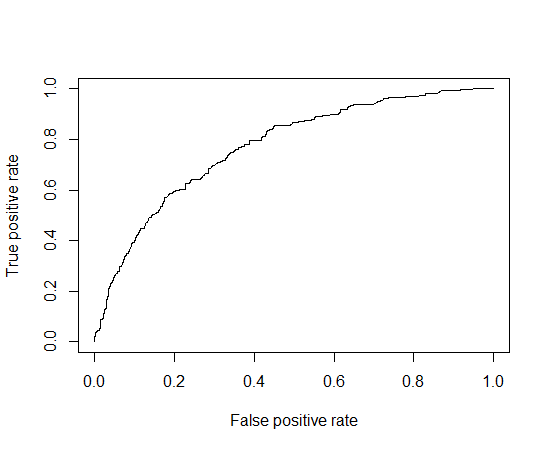

- AUC(area under curve): ROC curve 아래의 면적, 숫자가 높을수록 좋다.

- omission.rate: the ommission rate as a proportion of true occurrences misidentified given the defined threshold value

- sensitivity: 1일 확률, 민감도

- specificity: 0일 확률, 특이도

- prop.correct: 모델의 정확도

- kappa statistic

- Fleiss의 판단기준..

- 신뢰도 낮다: 0.4 미만

- 신뢰도 있다: 0.4 ~ 0.6

- 신뢰도 높다: 0.6 ~ 0.75

- 신뢰도 매우 높다: 0.75 초과

참고: 최적(정확도)의 threshold 찾기

for (i in seq(0,1,0.01))

{

rs <- c(rs, accuracy(x2$t0,x2$pred,threshold=i)$prop.correct)

}

max_val = max(rs)

for (i in seq(0,1,0.01))

{

tmp <- accuracy(x2$t0,x2$pred,threshold=i)$prop.correct

if ( max_val == tmp )

{

print (paste("threshold = ", i))

}

}

9 ROC(Receiver-Operating Characteristic curve) 곡선 #

install.packages("ROCR")

library("ROCR")

cname <- c("x1", "x2", "x3","x4", "x5", "x6", "y")

german = read.table("c:\\data\\german1.txt", col.names = cname)

options(contrasts = c("contr.treatment", "contr.poly"))

german.object <- glm(formula = y ~ x1 + x2 + x3 + x5, family = binomial, data = german)

pred <- predict(german.object, german, type="response")

logodds <- predict(german.object, german)

german <- cbind(german, pred)

german <- cbind(german, logodds)

roc = prediction(german$pred, german$y)

perf = performance(roc, "tpr", "fpr")

#"tpr"은 hit rate, "fpr"은 헛경보율(false alarm rate)

plot(perf)

#plot(perf, print.cutoff.at=seq(0,1,by=0.1))

install.packages("logistf")

library("logistf")

lr2 = logistf(y ~ x1 + x2 + x3 + x5, data = german)

summary(lr2)

결과

> summary(lr2)

logistf(formula = y ~ x1 + x2 + x3 + x5, data = german)

Model fitted by Penalized ML

Confidence intervals and p-values by Profile Likelihood

coef se(coef) lower 0.95 upper 0.95 Chisq

(Intercept) 0.64472876 0.474759083 -0.27043182 1.581359116 1.89900357

x1A12 -0.52660853 0.185120846 -0.88988344 -0.166823398 8.25198090

x1A13 -1.04548754 0.334474867 -1.72559520 -0.417128337 11.03319913

x1A14 -1.87794257 0.205266409 -2.28709164 -1.483111213 Inf

x2 0.03387929 0.006308928 0.02165981 0.046313848 29.94733537

x3A31 -0.09194231 0.473477203 -1.01911361 0.824239056 0.03855106

x3A32 -0.92696865 0.369386547 -1.66277580 -0.221680910 6.67102543

x3A33 -0.90779881 0.431809628 -1.76384501 -0.081117723 4.64170188

x3A34 -1.49870282 0.392307541 -2.27839153 -0.748208241 15.50420478

x5 -0.01252255 0.007063063 -0.02651766 0.001115517 3.23324577

p

(Intercept) 1.681899e-01

x1A12 4.070755e-03

x1A13 8.949457e-04

x1A14 0.000000e+00

x2 4.439416e-08

x3A31 8.443407e-01

x3A32 9.799279e-03

x3A33 3.120404e-02

x3A34 8.232193e-05

x5 7.215754e-02

Likelihood ratio test=200.5529 on 9 df, p=0, n=1000

Wald test = 152.8214 on 9 df, p = 0

Covariance-Matrix:

[,1] [,2] [,3] [,4] [,5]

[1,] 0.225396187 -2.116841e-02 -0.0178520944 -1.475598e-02 -1.030299e-03

[2,] -0.021168410 3.426973e-02 0.0158947775 1.663656e-02 -4.993463e-05

[3,] -0.017852094 1.589478e-02 0.1118734364 1.582290e-02 1.008258e-04

[4,] -0.014755985 1.663656e-02 0.0158228986 4.213430e-02 -6.926150e-05

[5,] -0.001030299 -4.993463e-05 0.0001008258 -6.926150e-05 3.980257e-05

[6,] -0.129133562 4.653294e-03 0.0017777035 2.271459e-03 1.822720e-04

[7,] -0.134642541 3.932850e-03 0.0010335670 1.458292e-04 2.134383e-04

[8,] -0.118628622 -2.470301e-03 0.0005935660 -5.484439e-03 -2.417103e-05

[9,] -0.126861265 4.418244e-03 0.0018526164 -2.134237e-03 2.052452e-04

[10,] -0.001743630 7.292805e-05 -0.0000437410 1.938701e-05 -1.300694e-07

[,6] [,7] [,8] [,9] [,10]

[1,] -1.291336e-01 -1.346425e-01 -1.186286e-01 -0.1268612649 -1.743630e-03

[2,] 4.653294e-03 3.932850e-03 -2.470301e-03 0.0044182436 7.292805e-05

[3,] 1.777704e-03 1.033567e-03 5.935660e-04 0.0018526164 -4.374100e-05

[4,] 2.271459e-03 1.458292e-04 -5.484439e-03 -0.0021342366 1.938701e-05

[5,] 1.822720e-04 2.134383e-04 -2.417103e-05 0.0002052452 -1.300694e-07

[6,] 2.241807e-01 1.258971e-01 1.240776e-01 0.1263132224 -8.388392e-05

[7,] 1.258971e-01 1.364464e-01 1.240557e-01 0.1260949748 7.408724e-05

[8,] 1.240776e-01 1.240557e-01 1.864596e-01 0.1247551153 -9.031551e-05

[9,] 1.263132e-01 1.260950e-01 1.247551e-01 0.1539052064 -1.431441e-04

[10,] -8.388392e-05 7.408724e-05 -9.031551e-05 -0.0001431441 4.988686e-05

이런거도 있다.

install.packages("survey")

library("survey")

regTermTest(german.object, ~x1 + x2 + x3 + x5)

결과

> regTermTest(german.object, ~x1 + x2 + x3 + x5)

Wald test for x1 x2 x3 x5

in glm(formula = y ~ x1 + x2 + x3 + x5, family = binomial, data = german)

F = 17.2046 on 9 and 990 df: p= < 2.22e-16

p-value가 조넨 작으니까 귀무가설 지지 못함. 즉, 차이가 있음.

german1.txt) 활용

german1.txt) 활용![[-]](/moniwiki/imgs/plugin/arrup.png "[-]")

![[+]](/moniwiki/imgs/plugin/arrdown.png "[+]")